Trace and access cover pays for finding a hidden leak and making good the access (floors, walls, driveways opened to reach it), not for fixing the pipe itself. 94% of buildings policies include it according to MoneySuperMarket, citing Defaqto, with typical limits of £5,000 to £10,000. Check your wording before work starts.

What Is Trace and Access Cover? Home Insurance Explained

A hidden water leak creates two very different bills. There is the damage the water has done, and there is the cost of finding the leak in the first place, which can mean opening floors, walls or a driveway just to reach the pipe. Trace and access cover exists for that second bill, and it is one of the most useful and least understood parts of a buildings insurance policy.

This guide explains what trace and access cover pays for, what it leaves out, the limits to expect, and how to use it properly when a leak turns up. If it is the detection method itself you want explained, the survey, the kit and how the leak actually gets found, that lives in our companion article on what trace and access is.

What this guide covers

What trace and access cover pays for

The clue is in the two words. Trace: the professional work of locating a hidden leak, whether that is a detection survey with acoustic, thermal and tracer gas equipment or, in the old-fashioned version, exploratory opening-up. Access: the cost of getting to the pipe and then making good afterwards, replacing the section of floor, plasterboard, tiling or driveway that had to come up.

In practice, a trace and access claim on a typical hidden leak covers:

- The leak detection survey

The specialist visit that pinpoints the leak, including the report that documents where it is and how it was found. - Opening up

Lifting floorboards or flooring, cutting plasterboard, breaking out a section of screed or lifting driveway surfacing to expose the pipe at the marked point. - Making good the access

Reinstating what was opened: reboarding, refixing flooring, patching screed, relaying the lifted surface. Making good covers the access point, not redecorating the whole room.

The logic from the insurer’s side is simple. Paying for a precise survey and one small hole is far cheaper than paying for a flooded kitchen six months later, or for three exploratory holes dug in the wrong places.

What trace and access does not cover

This is where claims go wrong, so it deserves plain language.

- The pipe repair itself

Fixing or replacing the leaking pipe is usually treated as maintenance and sits outside trace and access. On a straightforward leak the repair is often the cheapest line on the invoice, but it is normally yours. - The water damage

Ruined flooring, ceilings and decoration fall under the escape of water section of your policy, a separate peril with its own terms and excess. More on the difference below. - Wear-and-tear exclusions

If the insurer judges the pipework failed through long-term neglect or gradual deterioration you were aware of, parts of the wider claim can be reduced or declined. Acting quickly when signs appear protects you here. - Anything above the limit

Cover is capped. A complex commercial-scale excavation can exceed a £5,000 limit, so check the number before assuming everything is paid.

None of this makes the cover poor value. It just means trace and access is one piece of the claim, sitting alongside escape of water cover rather than replacing it.

How common is trace and access cover, and what are the limits?

The headline numbers come from MoneySuperMarket’s trace and access guide, which cites Defaqto’s analysis of UK buildings policies: 94% include the cover, and limits typically run from £5,000 to £10,000. So the odds are good that you already have it. The exceptions tend to be older policies, budget policies and some landlord products, which is why the first step in any leak situation is fifteen minutes with your policy document, searching the wording for “trace and access”.

One Scottish note worth adding: because most households here are unmetered, there is no water bill spike to flag a hidden leak early (Scottish Water explains why). Leaks tend to be found later, after visible damage appears, which makes the finding-the-leak cost, and this cover, more relevant in Scotland rather than less.

Trace and access vs escape of water: the difference in one table

| Trace and access | Escape of water | |

|---|---|---|

| What it pays for | Finding the leak and making good the access to it | Repairing the damage the escaped water caused |

| Covers the detection survey? | Yes, this is its core purpose | No |

| Covers the ruined ceiling and flooring? | No, only what was opened to reach the pipe | Yes, subject to policy terms |

| Covers the pipe repair? | Not usually | Not usually |

| Typical trip-up | Assuming it pays for everything leak-related | Gradual damage and wear-and-tear exclusions |

Most real claims use both sections together: trace and access funds the survey and the hole, escape of water funds the drying and reinstatement of damage. Our guide to whether home insurance covers water leaks covers the escape of water side, including the honest list of what gets excluded.

How to use trace and access cover in a claim

Step 1: Limit the damage first

Insurers expect you to act reasonably. If water is actively escaping, close the internal stop valve. Mitigation never harms a claim; leaving a known leak running does.

Step 2: Read your policy wording

Find the trace and access section, note the limit and the excess, and check whether the insurer requires you to use its approved contractors or lets you instruct your own leak detection specialist. Both models exist.

Step 3: Notify the insurer early

Report the suspected leak before commissioning major work where possible. If the leak is an emergency and you need detection immediately, keep every invoice and report; insurers routinely accept work done urgently, but they dislike surprises.

Step 4: Get the leak professionally located

A non-destructive survey pinpoints the leak and keeps the access small, which keeps the claim comfortably inside the limit. It also produces the document the insurer wants to see: a detection report.

Step 5: Keep the paper trail

Photographs of the damage, the detection report, invoices for the survey and the making good. The clearer the file, the faster the settlement.

If you are at step 4 and need a leak found anywhere in Scotland, call us on 07700 152 467. We work with insurance claims week in, week out, and our reports are written with loss adjusters in mind.

Where the detection report fits

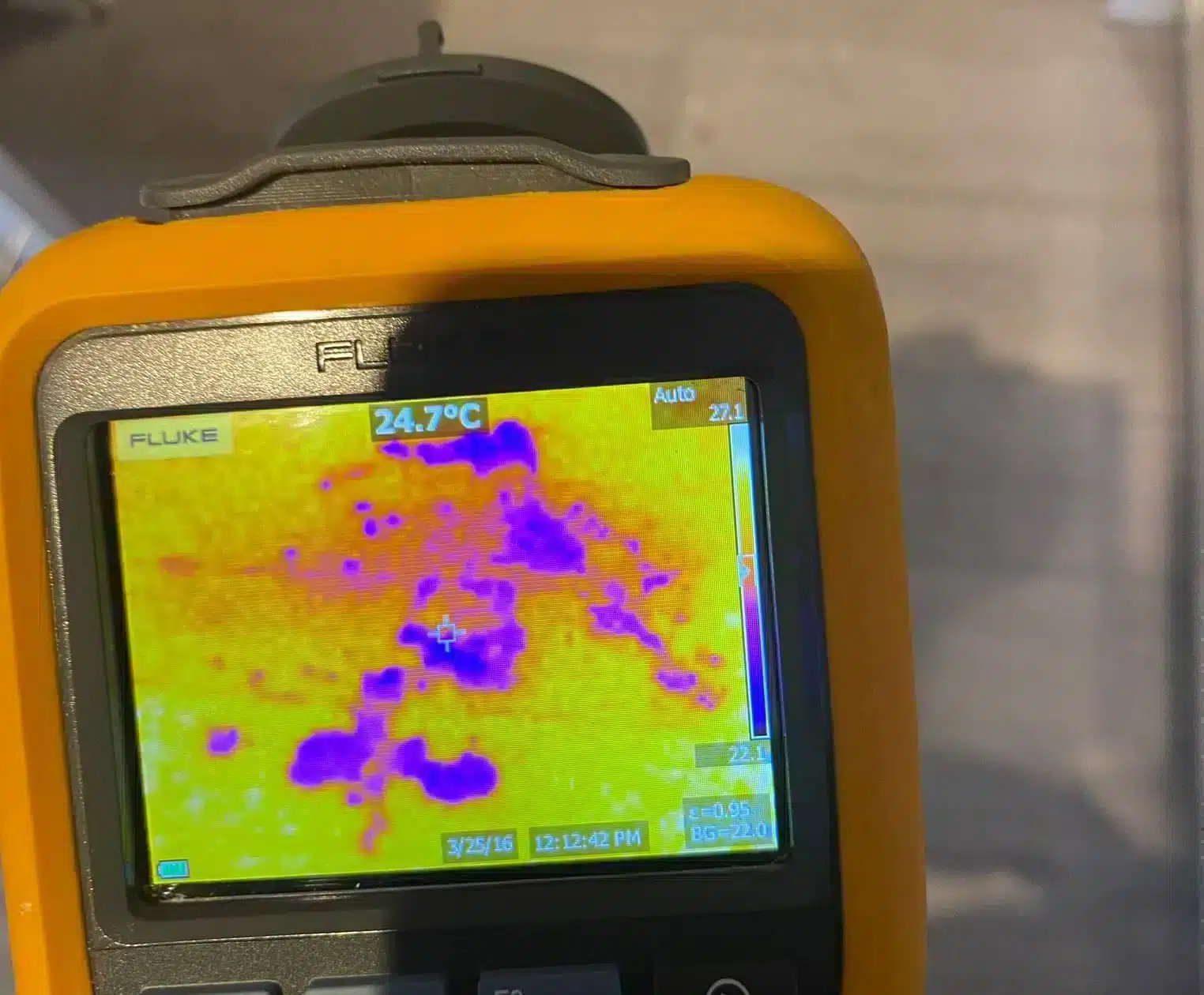

A professional detection report does two jobs in a trace and access claim. First, it proves the leak existed and was hidden, which is the trigger for the cover in the first place. Second, it documents exactly where the leak was, how it was located and what access was needed, which justifies the making-good costs.

Surveys use thermal imaging, acoustic listening and tracer gas to put a precise mark on the leak before anything is opened. The smaller and better-justified the access, the smoother the claim.

We explain what goes into these documents in our article on leak detection reports for insurance.

Frequently asked questions

Does trace and access cover pay to repair the leaking pipe?

Usually not. The cover pays to locate the leak and to make good whatever was opened up to reach it. The pipe repair itself is normally treated as the owner’s maintenance cost, and the resulting water damage falls under the escape of water section of the policy instead. Always confirm against your own wording.

Is trace and access included in every home insurance policy?

Most, but not all. MoneySuperMarket, citing Defaqto, reports that 94% of buildings insurance policies include trace and access cover. Older, budget and some landlord policies are the usual gaps, and limits vary between insurers, so check your schedule and wording rather than assuming.

How much trace and access cover do I have?

Typical limits run from £5,000 to £10,000 per claim, and the figure is stated in your policy schedule or wording. Domestic leaks located non-destructively rarely approach those limits, because a precise survey keeps the opening-up small. Large excavations or commercial pipework are where limits start to matter.

Can I choose my own leak detection company for a claim?

Often, yes. Some insurers send their own approved contractor, others are happy for you to instruct a specialist and submit the invoice and report under your trace and access cover. Check with your insurer first, and keep the detection report either way, since it supports the rest of the claim.

Will a trace and access claim still work if the damage is excluded?

It can. Trace and access and escape of water are separate sections, so an insurer may fund locating the leak and making good the access even where gradual damage exclusions reduce the damage payout. The detection report matters here too, because it establishes when and where the leak was found.

Related reading

- What Is Trace and Access? The Method Explained

- Does Home Insurance Cover Water Leaks? Escape of Water Explained

- How to Make a Water Leak Insurance Claim (Step by Step)

- Why Insurers Ask for a Leak Detection Report (and What’s in One)

MCR Leak Detection provides professional leak detection for insurance claims across Scotland.

Speak to MCR Leak Detection

If a hidden leak needs found for an insurance claim, we locate it non-destructively anywhere in Scotland, 24/7, and provide a clear detection report your insurer can work from.